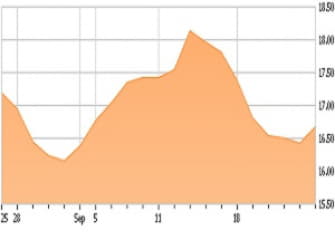

When Under Armour (NYSE:UA) (NYSE:UAA) reported second-quarter results last month, investors were hoping the company's stock was finally finding a bottom. The company had seen a plethora of negative news flood its ticker including "losing relevancy compared to a year ago" in the very important U.S. teen demographic, job cut announcement in the company's connected fitness business unit, and FBR Capital lowering their price target after recent channel checks. However, the stock moved lower as a result of the earnings release mainly due to management lowering the full year revenue forecast down to 9% to 11% growth compared to the previous 11% to 12% figure.

During the 2nd quarter, revenue increased 9% to $1.1 billion. The increase was primarily driven by a 20% increase in direct-to-consumer revenue, which is important because it will drive margins as this revenue stream gains in proportion to total revenue. Despite the higher direct-to-consumer sales, gross margin decreased further to 45.8% largely as a result of managing inventories. However, inventories continued to climb at an 8% rate, which indicates that there will likely be further markdowns as the company continues to manage inventories appropriate to market demand. This is apparent in the company's gross margin guidance for 2017 slightly lower than 2016's gross margin rate of 46.2%. The reasons for the lowered guidance primarily focus around simmering North American growth as consumer sentiment shifts and competition increases.

READ FULL ARTICLE HERE